Who Are the Foreign-Born Ultra Wealthy, And Why Should Organizations Pay Attention?

Written by Moira Boyle — Published by Altrata

The ultra wealthy are more entrepreneurial, more mobile, and more globally connected than ever before. Here is what Altrata’s new data on the foreign-born UHNW population reveals about where wealth is moving and how organizations can act on it.

The world’s ultra-wealthy are no longer anchored to a single country or market. They are building wealth across borders, operating across multiple jurisdictions simultaneously, and expecting the organizations that serve them to keep pace. Understanding who they are, how they built what they have, and where they are going has never been more commercially important.

That was the focus of our recent webinar, The New Dynamics of Global Wealth: Insights into Mobility and UHNW Opportunity, where I sat down with Maeen Shaban, Altrata’s Director of Research and Analytics, and Armand Arton, CEO and Chairman of Arton Capital, to unpack the findings from our latest report, Global Citizens: Entrepreneurship, Mobility and the Ultra Wealthy.

What follows are the most important takeaways from that conversation and what they mean for organizations seeking to engage this population.

Key takeaways

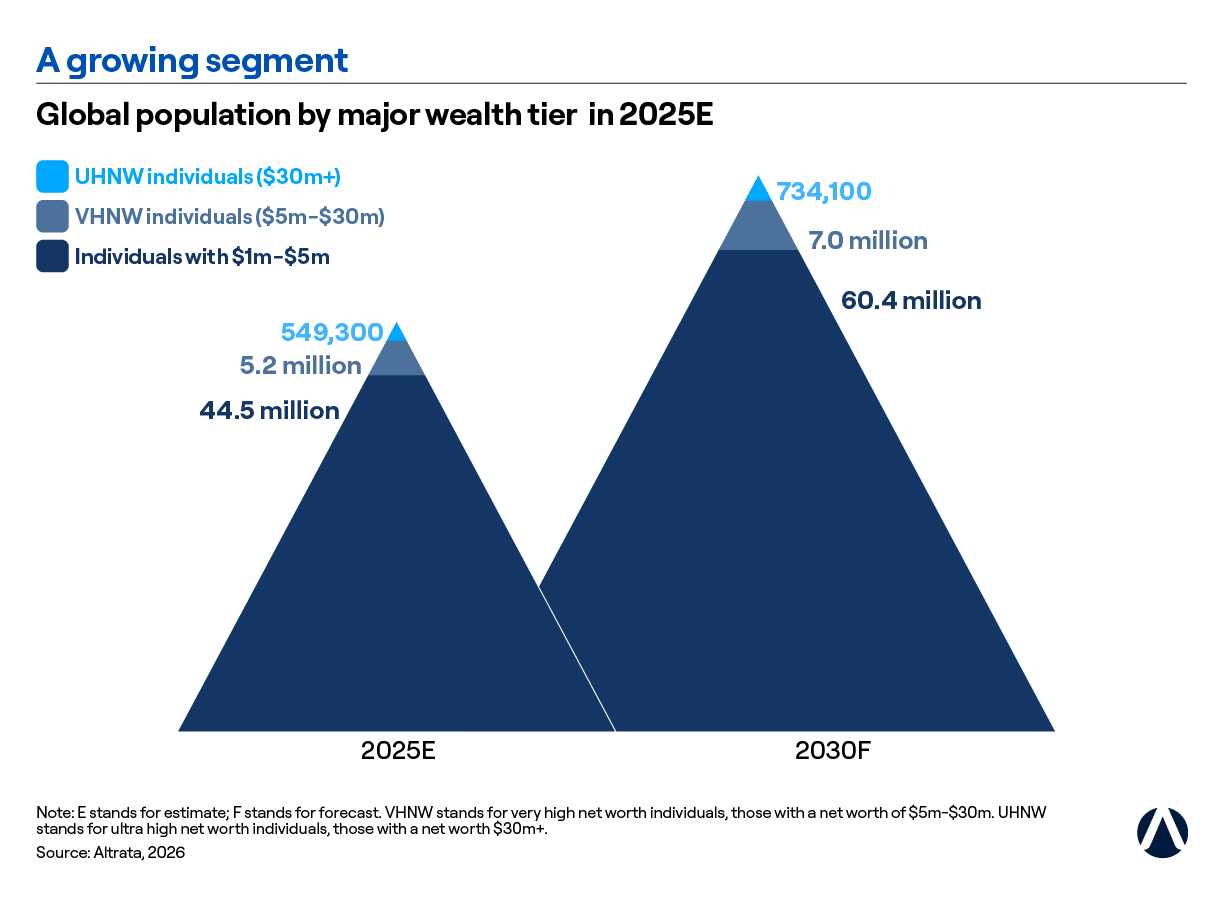

The scale is staggering, and it is still growing.

There are nearly 550,000 UHNW individuals globally today, collectively controlling more wealth than the combined GDP of the United States and China. By 2030, that population is forecast to reach 734,000 individuals with $84 trillion in combined wealth. The foreign-born cohort, roughly one in five, punches well above its weight and is growing alongside it.

This is a self-made, entrepreneurial cohort, not inherited wealth.

80% of foreign-born ultra-wealthy individuals are entirely self-made. Three quarters have held CEO or founder roles. These are active wealth builders, not passive inheritors, which means they have different risk profiles, different expectations, and a fundamentally different engagement model than the archetypes organizations have historically planned around.

One client, five jurisdictions.

Armand Arton shared that the typical global citizen operates across at least five jurisdictions simultaneously, balancing where their children study, where they conduct business, where they hold property, and where they are planning their legacy. This is not occasional international travel. It is a genuinely global lifestyle, and it demands a new approach to clienteling, marketing, and service delivery.

Each hub tells a different story and requires a different strategy.

The four major UHNW hubs we examined, the US, Dubai, London, and Singapore, each attract a distinct profile. The US draws self-made tech and venture capital entrepreneurs. Dubai skews younger, with one in five foreign-born wealthy individuals under 50. London is defined by its concentration in financial services. Singapore attracts older, wealth-preservation-focused individuals from China, India, and emerging Southeast Asian markets. Knowing which hub your clients call home tells you a great deal about how to engage them.

The opportunity is in hyper-segmentation, not broad strokes.

According to Boston Consulting Group’s 2024 True-Luxury Global Consumer Insights report, a single ultra-wealthy consumer represents approximately 230 times the value of one aspirational consumer. The organizations winning in this space are not casting wide nets. They are identifying and engaging specific subsets with precision. The global citizen is now one of the most clearly defined and actionable segments in wealth intelligence, and the data exists to build a real strategy around it.

The destinations to watch are already moving.

Beyond the established hubs, Armand flagged several markets gaining momentum quickly with the UHNW set. Italy and Milan have surged in popularity, first with post-Brexit British wealth, then with Gulf-region families drawn to Italy’s competitive flat tax rate. Argentina is emerging as a potential breakout destination, with economic citizenship expected to be introduced and improving fundamentals reshaping its appeal. New Zealand and Cape Town are increasingly viewed as contingency locations by families seeking geopolitical distance and stability in an uncertain world.

The headlines are compelling on their own. But the data behind them tells an even richer story. Here is what we covered in the session.

UHNW population growth: why the ultra wealthy are the most valuable segment

To set the stage, Maeen walked us through the current state of the global UHNW population: individuals with a net worth of $30 million or more. At the end of 2025, that population stood at just below 550,000 people worldwide, roughly the population of Edinburgh, yet together they control $63 trillion in wealth. That figure exceeds the combined GDP of the United States and China.

And it is not a static picture. By 2030, Altrata’s data forecasts this population will grow by roughly a third, reaching approximately 734,100 individuals with a combined wealth of $84 trillion. The forces driving that growth include continued digital innovation, the accelerating rise of AI and technology-driven wealth creation, and a generational wealth transfer that is putting capital into new hands at an unprecedented pace.

For organizations across financial services, luxury, nonprofits, and beyond, this is not background context. It is the foundation of every commercial and engagement strategy.

The foreign-born ultra wealthy: behaviors, networks, and cross-border opportunity

The central finding of the report, and the thread that ran through our entire discussion, is this: nearly one in every five UHNW individuals is foreign-born. These are people who were born in one country and have built their wealth, their careers, and their lives in another.

Maeen was careful to define what we mean: this is not about second homes or occasional international travel, these are individuals who have genuinely relocated and created wealth in a country different from the one they were born in. They are first-generation movers and one of the most commercially distinct behavioral segments we can identify.

What makes this group so significant is not just their size. It is their behavior. More than a third studied outside their birth country, often laying the groundwork for the cross-border networks and market exposure that would define their careers. Roughly one in five holds a stake in a business headquartered outside their primary country of residence. These are not passive investors. They are actively building and co-owning companies across multiple jurisdictions simultaneously.

As Maeen put it, the modern UHNW individual no longer thinks in terms of a single home market. They think in terms of optionality: where is the best opportunity, where can they operate most freely, where can they protect and grow what they have built.

The rise of self-made ultra wealthy individuals and what it means for engagement

Perhaps the most striking data point from the report is this: 80% of the foreign-born UHNW population are entirely self-made. Four in five individuals with $30 million or more built that wealth from scratch, in a country that was not their own.

That is a fundamentally different profile from the inherited wealth archetypes that have historically defined how organizations think about the ultra wealthy. The old model of land, legacy, and dynastic family wealth is giving way to something more dynamic. These are founders and CEOs, people who have held leadership roles and taken on significant risk in pursuit of wealth creation. Three quarters of the foreign-born ultra wealthy have been CEOs at some point in their careers, and many have held founder roles.

“The modern UHNW individual no longer thinks in terms of a single home market. They think in terms of optionality.”

Armand validated this picture from his own vantage point. Arton Capital has worked with more than 20,000 families over 20 years, advising on residency and citizenship by investment across 12 jurisdictions. The vast majority of those clients, he told us, are first-generation, self-made wealth holders who are thinking not just about their own financial success but about the legacy of freedom they want to pass to the next generation. Mobility, he said, has become as important a form of inheritance as financial capital.

UHNW wealth hubs: how the ultra wealthy population differs globally

In the session we covered four distinct wealth hubs, each with a different profile of the foreign-born UHNW population.

The United States remains the world’s dominant wealth market, home to approximately 205,000 ultra-high-net-worth individuals, nearly 40% of the global total. The foreign-born cohort there mirrors the broader self-made profile closely, with strong representation in venture capital, technology, and life sciences. The US has long been the destination for ambitious, risk-tolerant wealth builders, and the data confirms that dynamic continues.

Dubai tells another story. It has transformed rapidly from a regional financial hub into a global wealth center, and it is attracting a younger cohort. One in five foreign-born wealthy individuals in Dubai is under 50, a proportion three times higher than in Singapore. The wealth profile is also different, with roughly 40% having a combination of self-made and inherited wealth, and the industry spread is notably diverse, with no single sector dominating.

London is shaped by one industry above all others. Nearly half of London’s foreign-born ultra-wealthy built their wealth in banking and financial services. That is more than double the global average. Brexit and non-domiciled residency changes have created friction. But London’s legal stability, cultural depth, and elite education ecosystem keep it compelling.

Singapore rounds out the picture as the most mature destination in the group. The foreign-born cohort there skews older, with two in five over 70. Financial services dominates, accounting for roughly a third of the population. Singapore draws wealth primarily from China and India, as well as emerging Southeast Asian markets. It is a dependable, long-term destination for wealth preservation.

What ties all four together, as Maeen noted, is that each is actively and deliberately competing for globally mobile capital. The difference lies in who they attract, shaped by regulatory environment, economic structure, tax policy, and lifestyle proposition.

It’s time to rethink your UHNW engagement strategy

One question ran through the entire session. What does this mean for organizations trying to engage this population?

A few themes emerged clearly:

Hyper-segmentation is no longer optional.

The UHNW population is not a monolith, and the foreign-born segment makes that even more pronounced. A client operating across five jurisdictions, as Armand noted, is not the same as a domestically-focused ultra-wealthy individual. Their needs, behaviors, and expectations of providers are different in ways that matter commercially.

Context determines everything.

As Maeen explained, knowing a client’s hub, industry, and life stage changes the entire nature of how you engage them. A 50-year-old entrepreneur in Dubai has different priorities than a 70-year-old preservationist in Singapore. Generic engagement strategies will miss both.

Behavior signals opportunity.

Armand noted that business activity follows personal mobility. Clients who establish residency in a new country often bring their corporate interests within months. Organizations that understand the individual, their network, and their trajectory will be better positioned to serve them.

Turning UHNW wealth intelligence into advantage

The ultra wealthy are not just growing in number. They are growing in complexity, global reach, and in what they expect from the organizations that serve them. One in five is a foreign-born global citizen building wealth across borders. Four in five of that group are entirely self-made. They are entrepreneurial, mobile, and interconnected in ways our data, for the first time, makes visible.

The commercial weight of this population is difficult to overstate. According to BCG’s 2024 True-Luxury Global Consumer Insights report, one ultra-wealthy consumer is worth 230 times an aspirational consumer. That ratio alone should reframe where luxury, wealth management, and nonprofit organizations focus their resources.

That is the opportunity. And it is significant.

For wealth managers, it means the intelligence to identify and qualify high-net-worth prospects before the competition does. In terms of luxury brands, it means the context to personalize engagement across borders and life stages. And when we’re talking about nonprofit organizations, it means the insight to find and cultivate major donors with the capacity and propensity to give. But none of that is possible without a deep, accurate understanding of who these individuals are and what drives them.

That is what Altrata is built to deliver. Our wealth intelligence platform delivers hand-curated, human-verified data on the world’s wealthiest individuals. It gives organizations the foundation to engage with confidence.

The data exists. The opportunity is clear. If you are ready to act on it, we would love to start that conversation.

Explore the fullGlobal Citizens report or access the on-demand recording to go deeper on the findings.

Join the conversation at Superyacht Summit Türkiye on 4–5 November 2026, where industry leaders will discuss the opportunities, challenges, and future direction of yachting across the Mediterranean and beyond.